Reporting Highlights

- Dialing for Dollars: America’s largest insurers hire EviCore to make decisions on whether to pay for care for more than 100 million people.

- “The Dial”: EviCore uses an algorithm that allows it to adjust the chances that company doctors will screen prior authorization requests, increasing the possibility of denials.

- Lucrative Deals: Some EviCore contracts are based on how deeply the company can reduce spending on medical procedures. It tells insurers that it can provide a 3-to-1 return on investment.

These highlights were written by the reporters and editors who worked on this story.

Every day, patients across America crack open envelopes with bad news. Yet another health insurer has decided not to pay for a treatment that their doctor has recommended. Sometimes it’s a no for an MRI for a high school wrestler with a strained back. Sometimes for a cancer procedure that will help a grandmother with a throat tumor. Sometimes for a heart scan for a truck driver feeling short of breath.

But the insurance companies don’t always make these decisions. Instead, they often outsource medical reviews to a largely hidden industry that makes money by turning down doctors’ requests for payments, known as prior authorizations. Call it the denials for dollars business.

The biggest player is a company called EviCore by Evernorth, which is hired by major American insurance companies and provides coverage to 100 million consumers — about 1 in 3 insured people. It is owned by the insurance giant Cigna.

A ProPublica and Capitol Forum investigation found that EviCore uses an algorithm backed by artificial intelligence, which some insiders call “the dial,” that it can adjust to lead to higher denials. Some contracts ensure the company makes more money the more it cuts health spending. And it issues medical guidelines that doctors have said delay and deny care for patients.

EviCore and companies like it approve prior authorizations “based on the decision that is more profitable for them,” said Barbara McAneny, a former president of the American Medical Association and a practicing oncologist. “They love to deny things.”

EviCore says it scrutinizes requests to make sure that procedures recommended by doctors are safe, necessary and cost-effective. “We are improving the quality of health care, the safety of health care and, by very happy coincidence, we’re also decreasing a significant amount of unnecessary cost,” an EviCore medical officer explains in a video produced by the company.

But EviCore’s cost-cutting is far from coincidental, according to the investigation.

EviCore markets itself to insurance companies by promising a 3-to-1 return on investment — that is, for every $1 spent on EviCore, the insurer would pay out $3 less on medical care and other costs. EviCore salespeople have boasted of a 15% increase in denials, according to the investigation, which is based on internal documents, corporate data and dozens of interviews with former employees, doctors, industry experts, health care regulators and insurance executives. Almost everybody interviewed spoke on condition of anonymity because they continue to work in the industry.

An analysis of the company’s own data shows that, since 2021, EviCore turned down prior authorization requests, in full or in part, almost 20% of the time in Arkansas, which requires the publication of denial rates. By comparison, the equivalent figure for federal Medicare Advantage plans was about 7% in 2022.

They love to deny things.

EviCore has several ways to cut costs for insurers. Chief among them is the dial, the proprietary algorithm that’s the first stop in evaluating a prior authorization. Based on data entered by a doctor’s office, it can automatically approve a request.

The algorithm cannot say no, however. If it finds problems, it sends the request for review to a team of in-house nurses and doctors who consult company medical guidelines. Only doctors can issue a final denial.

This is where tweaking the dial comes in. EviCore can adjust the algorithm to increase the number of requests sent for review, according to five former employees. The more reviews, the higher the chance of denials.

New here?

We’re ProPublica, a nonprofit, independent newsroom with one job: to hold the powerful to account. Here’s how we’re reporting on democracy this election season:

We revealed how Ziklag, a secret organization of wealthy Christians including the families behind Hobby Lobby and Uline, is spending millions to try to sway the election and change the country.

We’re trying something new. Was it helpful?

Here’s how it works, the former employees said: The algorithm reviews a request and gives it a score. For example, it may judge one request to have a 75% chance of approval, while another to have a 95% chance. If EviCore wants more denials, it can send on for review anything that scores lower than a 95%. If it wants fewer, it can set the threshold for reviews at scores lower than 75%.

“We could control that,” said one former EviCore executive involved in technology issues. “That’s the game we would play.”

Over the years, medical groups have repeatedly complained that EviCore’s guidelines were outdated and rigid, resulting in inappropriate denials or delays in care. Frustration with the rules has led some doctors to refer to the company as EvilCore. There is even a parody account on X.

The guidelines are also used as a tool to cut costs, the investigation found. Company executives “would say, ‘Keep a closer eye on the guidelines for reviews for a particular company because we’re not showing savings,’” said a former EviCore employee involved in the radiation oncology program.

EviCore says that it develops its guidelines with the input of peer-reviewed medical studies and professional societies, and that they are routinely updated to stay current with the latest evidence-backed practices. It said its decisions are based solely on the guidelines and are not interpreted differently for different clients.

EviCore is not alone in engaging in the denials-for-dollars business. The second-biggest player is Carelon Medical Benefits Management, a subsidiary of Elevance Health, the health insurer formerly known as Anthem. It has been accused in court of wrongfully denying legitimate requests for coverage. The company has denied all charges. Several smaller companies do the same kind of work.

Simply put, EviCore uses the latest evidence-based medicine to ensure that patients receive the care they need and avoid the services they do not.

There is no question that prior authorizations play an important role in modern medicine. They serve to guard against doctors who recommend unnecessary and even potentially harmful treatments. They also protect insurers from fraudulent physicians who overbill for services.

In a response to questions, a Cigna spokesperson provided a statement on behalf of EviCore. “Simply put, EviCore uses the latest evidence-based medicine to ensure that patients receive the care they need and avoid the services they do not,” it said.

The statement acknowledged that EviCore used algorithms for some clinical programs, but “ONLY to accelerate approval of appropriate care and reduce the administrative burden on providers.”

The statement noted that doctors have the ability to appeal prior authorization denials, and that the company routinely monitors the outcomes “as part of our continuous quality improvement to ensure accurate and timely medical necessity decision-making.”

Prior authorization reviews provided by EviCore save money for the entire health insurance system, the statement said. “The natural product of improved care quality and reduced waste is savings for our clients, lower out-of-pocket costs for patients, and fewer health care premium increases for Americans.”

Turning the Dial

In the fall of 2021, when the air grew crisp and the leaves reddened in central Ohio, Little John Cupp began feeling short of breath. He gasped while pushing a shopping cart. His feet and ankles swelled. He could only sleep while sitting up.

An echocardiogram revealed that his heart was having trouble pumping blood. Cupp’s doctor suggested more testing, including the insertion of a catheter to examine whether his arteries were blocked.

A few days after the doctor made the request, Cupp received a letter from his insurance company, UnitedHealthcare. The procedure, it said, was “not medically necessary.”

One sentence in 8-point type revealed that the insurer had outsourced the decision to EviCore.

Cupp’s doctor put him on medications to reduce swelling and high blood pressure and tried a second time to win approval for a left heart catheter examination. EviCore turned it down again. He revealed his disappointment in shorthand in Cupp’s medical records: “ideally he needs LHC (denied twice by insurance).”

Cupp was 5-foot-7 and 282 pounds, with a wedding ring the size of a quarter. He had a white beard, his face wide and warm. He wore blue jean overalls and scuffed leather work boots. He had spent most of his life as a welder, working at metal fabrication shops in and around his hometown of Circleville, Ohio, population 14,063. He was 61, nearly the same age as his father when he died from a massive heart attack. Cupp was a stoic, his daughter Chris said, but the denial worried him.

“Well, I have to call the doctor and see what we’re going to do,” he told her after the second rejection.

The doctor decided to give up on getting an approval for the catheter exam. In challenging EviCore, he was fighting not just a company but an industry.

EviCore is the product of a massive, decadeslong push by insurance companies to control health care costs. They point to studies that show 20% to 45% of some medical treatments are wasteful or ineffective. To decrease such spending, insurers began requiring doctors to seek permission for medical care before agreeing to pay for it — a process known as “utilization review.” As treatments became more complex, the reviews proved costly in themselves.

Created from a 2014 merger of two smaller companies, EviCore offered a solution: It allowed insurers to outsource prior authorization decisions for the most specialized and expensive procedures. EviCore today issues recommendations for imaging, oncology, cardiology, gastroenterology, sleep problems and many other fields.

It works with more than 100 insurers across the country, including industry titans such as UnitedHealthcare, Aetna and Blue Cross Blue Shield and some Medicare and Medicaid contractors. Cigna took over the company in 2018, but EviCore maintains its independence by blocking insurers from prying into one another’s proprietary data.

In responses to inquiries, the large insurance companies said they hired EviCore as a way to make sure that customers received safe and necessary medical treatments, while holding down costs for inappropriate care.

EviCore built its business by relying on different types of contracts. In one, a health insurance company pays EviCore a flat rate to review coverage requests.

Another type is more lucrative, providing an incentive for EviCore to cut costs, former employees said. Known as risk contracts, EviCore takes on the responsibility for paying claims. As an example, say an insurer spends $10 million a year on MRIs. If EviCore keeps costs below that figure, it pockets the difference. In some cases, it splits the savings with the insurance company.

“Where you really made your money was on a risk model,” a former EviCore executive said. “Their margins were exponentially higher.”

EviCore teams involved in developing the algorithms and contracting with clients “operate separately” from reviewers “to prevent any potential conflicts of interest,” according to the statement from Cigna’s spokesperson.

Insurers do not make explicit demands for more denials, a former EviCore sales executive said, Instead, they asked about “controlling the spend” — the amount of money paid out on certain procedures, he said. Nor would EviCore always use the word “denials” — they employed circumlocutions like “inappropriate determinations.”

Aetna and Cigna are two of the companies that have requested “high touch” plans — those that would send more cases to clinical review and thus generate more denials, according to the former employee involved in data issues.

Aetna did not directly respond to whether it used “high touch” plans. “Although we never automate medical necessity denials, we automate and provide real-time approval of some services to ease administrative burden and allow providers to focus on patient care,” the insurer said in a statement. Cigna did not respond to questions about its use of such plans.

The fact that these big companies focused on profits and can play all these games is quite disturbing to me.

“When you have human eyes on something, you can pick up where there might be a gray area where the algorithm might not pick up,” a former EviCore account executive said. “That is how you would increase the denial rate.”

EviCore can also adjust the algorithm to achieve its internal goals, without the knowledge of clients, former employees said. This happened when EviCore was not generating enough savings to demonstrate its value to insurers, several former employees told ProPublica.

“The pressure from our business leaders was to make sure that we were able to provide evidence of a strong enough impact to justify the contracts with clients,” said the former employee involved with technology.

The system also runs in reverse. When doctors or employer health plans complain about high rejection rates, insurance companies can ask EviCore to back off. The company simply adjusts its algorithm to approve more prior authorization requests.

Dave Jones, a former California insurance commissioner and now director of the climate risk initiative at the University of California, Berkeley School of Law, said arbitrarily increasing or decreasing manual reviews didn’t appear to violate any standards. Still, he questioned whether a payment structure or contract for EviCore based on reducing claims payments or authorizations would result in objective and thorough evaluations of prior authorization requests, as required by law.

“That to me is troubling,” Jones said. “It suggests that the claim settlement procedure is not objective, right?” He added, “It calls into question everything that’s occurring.”

Other industry experts found the manipulation of denial rates upsetting.

“The fact that these big companies focused on profits and can play all these games is quite disturbing to me,” said Martin Lustick, a former insurance executive and the author of a book on industry practices. “They know the more reviews they do, the more denials they get.”

Disputed Guidelines

On March 2, 2022, Cupp and his daughter entered the Adena Regional Medical Center, a gray and glass building surrounded by central Ohio’s low rolling hills.

It had been almost three months since EviCore first turned down coverage for the catheterization. Changing tack, Cupp’s doctor ordered a new exam, which EviCore approved, called a nuclear stress test. It shows how well blood flows through your heart.

A heart catheterization generally costs around $3,500 when done in network, according to Fair Health, a nonprofit that tracks health care prices. A nuclear stress test runs about $315.

Afterward, Cupp greeted Chris in the waiting room. He told her he felt fine. They went for lunch at a favorite hamburger spot. At the time, they did not know the results of the stress test, which showed that his heart was pumping even less blood than indicated by his echocardiogram.

At each step of the way, EviCore had steered Cupp’s medical treatment by denying or approving his doctor’s coverage requests based on its own internal guidelines.

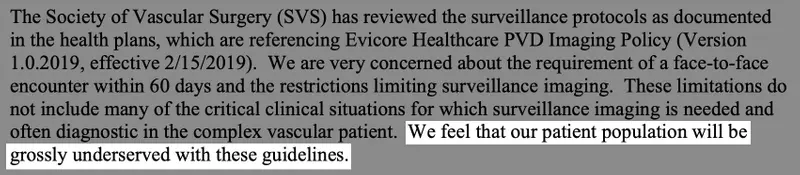

Those guidelines have long been the subject of complaints from doctors. Over the past five years, organizations ranging from the American College of Cardiology to the Society for Vascular Surgery to ASTRO, the American Society for Radiation Oncology, have written to EviCore or regulators that the guidelines are flawed and can interfere with delivering the right care for patients. Benjamin Durkee, a doctor who chairs ASTRO’s payor relations committee, said EviCore had generally made “a good faith” effort to respond to the society’s concerns. But, he noted, the company continues to consistently deny a radiation treatment called proton beam therapy for some pelvic tumors that is more costly but supported by ASTRO’s recommendations.

A 2023 academic study examined the criteria EviCore used to approve payment for imaging of the lower spine in cases of extreme pain. It found the guidelines deficient. Two of five medical experts who reviewed the guidelines even recommended not using them.

A 2018 audit by the Centers for Medicare and Medicaid Services, obtained through the Freedom of Information Act, found that Health Care Service Corporation, a Blue Cross Blue Shield insurer, had hired EviCore to review prior authorizations. EviCore, the audit found, played a role in making “inappropriate denials” for 30 patients because it failed to keep its cancer guidelines up to date. As a result, EviCore retrained its staff. HCSC did not respond for comment.

Former employees have also questioned how the guidelines were put to use.

A maternal-fetal medicine physician in Colorado, Gail Miller, took a job as a doctor at EviCore in 2018. The idea of ensuring safe medical practices appealed to her. But she soon grew convinced that EviCore was more interested in saving money.

EviCore rejected her suggestions for improving its maternal fetal health guidelines. Her supervisor required her to decide at least 15 cases an hour — or one every four minutes. She often reviewed requests by physicians outside her specialty.

Nine months after starting at EviCore, Miller quit, disappointed by the attitudes of some of her colleagues. “Most of the physicians who work at these places just don’t care,” she said. “Any empathy they had is gone.”

EviCore noted its clinical staff had “high engagement, satisfaction and retention rates.” It said the most common reason for denying a prior authorization is because doctors neglect to include necessary information.

Results

EviCore meets regularly with insurers and state Medicaid programs. It is a critical part of the business. The company has to demonstrate savings or clients will have little reason to continue their contracts.

Typical was a 2019 meeting with Vermont’s Medicaid program, which for years had used EviCore to review coverage requests for advanced radiology and cardiology scans. A slide show demonstrated how the company had helped lower costs for cardiac imaging through denials. Rates had zigzagged, from a high of almost 15% of requests in one three-month period to a low of 6.1% in another.

But the presentation, obtained through Vermont’s Public Records Act, revealed another way that EviCore saved money for insurers. Prior authorization requests for radiology imaging services had dropped to 3,629, a decline of 16%. Cardiology requests had plummeted even more — down 38% in a little more than a year. Doctors had simply stopped asking for procedures for their patients.

An EviCore executive called this the “sentinel effect” at a legislative hearing in Kansas. It is like the sheriff coming to town. Once doctors know EviCore is watching, they make fewer inappropriate prior authorization requests, he said.

Doctors, however, say that such decreases reflect how difficult it is to fight EviCore and similar companies. Their entrance into the market frustrates doctors from making otherwise legitimate requests.

In its statement, Cigna described the sentinel effect differently. The company said that it helps doctors stay up to date on best practices. “Sentinel effect refers to the reduction in frequency with which physicians order inappropriate services because they are now aware of the latest clinical evidence,” the statement read.

A spokesperson for Vermont’s Medicaid program said the state does not believe that EviCore made unfair or unsound coverage recommendations. Instead, EviCore helped Vermont make “sound decisions from both a fiscal and patient care perspective.”

“It is never a goal for the state of Vermont or our third-party contractors to deny service,” said Alex McCracken, spokesperson of Department of Vermont Health Access. “We are committed to delivery of service for our customers.”

Vermont eventually ended its contract with EviCore because it decided to no longer require prior authorization for advanced imaging scans in its Medicaid program.

“Too Much Say”

The day after his stress test, Cupp drove to his granddaughter’s high school to drop off her archery bow — it had been left behind in the morning rush. He and his wife went shopping at the grocery store. That evening, he watched as his grandkids showed off some baby frogs they had purchased at a pet store.

He went to bed at 8:30 p.m. in order to wake at 2:30 a.m. for the hourlong drive to his job as a maintenance worker at a medical supplies warehouse just south of Columbus.

At about 10:30 p.m., Cupp’s wife, Vivian, shook Chris awake. “Your dad’s breathing funny,” she told her. Chris ran into their bedroom. Her father was gasping for air. Suddenly, he stopped. Chris began CPR. She told her mom to call 911.

By the time the ambulance arrived at Adena Regional Medical Center, where he had received his nuclear stress test 36 hours earlier, his body was mottled and cool. He had suffered cardiac arrest. The time of death was 11:39 p.m.

ProPublica asked four cardiology experts to review Cupp’s medical situation. One cardiologist said she would not have recommended a heart catheterization. Given his symptoms, which did not include complaints about chest pain, the best diagnostic tool would have been the stress test, she said.

Three others said the heart catheterization was appropriate. One cardiologist noted that Cupp was diabetic, overweight and showed signs of having suffered a prior heart attack. “It’s very reasonable to say we’ll just go straight to a heart catheterization,” the cardiologist said.

If Cupp had received the procedure when first ordered, his life may have been saved, one expert said. “The doctor was absolutely right to order the catheterization. It was certainly necessary,” said Jonni Cooper, president of American Board of Cardiovascular Medicine and a board certified cardiovascular nurse practitioner.

State and federal regulators rarely impose onerous penalties on companies like EviCore.

Connecticut’s Insurance Department recently reviewed EviCore and Carelon. It found no problems with Carelon. EviCore was fined $16,000 this year for more than 77 violations found in a review of 196 files. EviCore is also accredited by two trade associations, which review companies periodically for compliance with industry standards.

Holding the companies legally responsible for their decisions is also difficult. In 2022, Carelon settled a lawsuit for $13 million that alleged the company, then called AIM, had used a variety of techniques to avoid approving coverage requests. Among them: The company set its fax machines to receive only 5 to 10 pages. When doctors faxed prior authorization requests longer than the limit, company representatives would deny them for failing to have enough documentation. Carelon denied the allegations in court and admitted no fault. A spokesperson declined to comment on the lawsuit.

Elevance, Carelon’s parent company, said its subsidiary “is focused on improving health outcomes while also lowering the cost of care.”

This year, Chris, representing Cupp’s estate, sued United Healthcare, EviCore, the Adena Regional Medical Center and Cupp’s doctor, accusing them of malpractice, among other allegations. Cupp’s attorney, John Markus, later decided to drop United and EviCore. Lawsuits against employer-funded health plans, like the one Cupp had with United, must be tried in federal court, where case law favors insurance companies. For instance, insurers found at fault do not pay punitive damages, only the cost of treatment. The medical center and the doctor declined to comment, citing the ongoing litigation. In court, both denied any wrongdoing. United and EviCore declined to discuss Cupp’s case, despite an offer from Chris to sign a waiver of medical privacy rights.

Her father’s death wracked Chris. He had been her best friend. He helped raise her three kids. He provided for the family. Two years before his death, he purchased a new double-wide trailer to replace a rusting single-wide the family had lived in for years. It had four bedrooms, enough for everyone. It stood on the side of a hill, surrounded by oak and maple, a leafy retreat with a view of the valley below.

Cupp was buried at a cemetery across from a cornfield on March 9. A gray granite headstone marks his date of death.

Chris Cupp drives a school bus to make ends meet. For extra pay, she picks up a lot of the trips for night games. She says she hopes that no one else has to go through what she did.

“Insurance has too much say over something that can save your life,” she said. “When it comes to your heart, something that’s going to kill you, they have too much say in that. That’s my thought about it.”

Do You Have Insights Into Dental and Health Insurance Denials? Help Us Report on the System.

Insurers deny tens of millions of claims every year. ProPublica is investigating why claims are denied, what the consequences are for patients and how the appeal process really works.

Agnel Philip contributed reporting.